The construction industry started in 2000-4000 BC when humans abandoned nomadic lifestyles and built shelters. The automobile, in its current shape and form, was invented in the 1860s. The construction industry in the USA is over $2 trillion, while the automotive industry is at $1 trillion.

However, it is fascinating that the ancient industry is far behind the automotive industry in adopting robotics. The construction industry comprises manufacturing, supply chain, design, project management, and onsite construction. Most physical activities of construction are done in the manufacturing and onsite construction facets. However, not all aspects of the construction industry are devoid of robotic automation. While some parts of manufacturing remain dependent on physical labor, other portions rely heavily on robotics, such as manufacturing of construction materials and prefabricated components. Onsite construction has been slow to adopt robotics. This writeup will focus on our insights regarding the challenges of onsite robotics.

It is not true that individuals in the construction industry lack resourcefulness, or adaptability. Many chemical and mechanical products frequently see fast adoption due to its clear value propositions. Construction workers need to be resourceful and quick problem-solvers because the work of construction can be very unpredictable on a daily basis. The point is that the construction industry is unique, and achieving significant advancements in robotics automation requires cooperation from various entities like construction and robot companies, investors, governments, and customers. It’s a process that requires patience, a collective effort, and innovation and engineering very focused on the construction companies and worker’s needs .

To understand why this is challenging, let’s look at the details.

A mature industry with lower margins and lack of strong monopoly

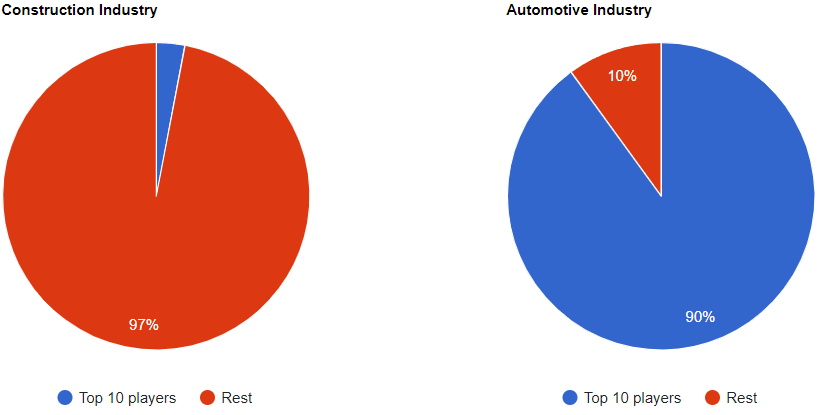

One challenge of the construction industry may be its maturity and equitable distribution compared to other monopolistic sectors. In the diagram below you can see that in the automotive industry the top 10 industry players by size control 90% of the industry. Compare that to the construction industry where the top 10 companies only control about 3% of the industry. In the automotive industry one contract with a major player can be sufficient for a company to themselves become a major player. This distribution of companies across construction means that establishing standards for construction robots is very difficult.

Data Courtesy: https://www.ibisworld.com/global/market-size/global-car-automobile-manufacturing

Further, the profit margins in both construction and automotive industries are low, below 10%. However, for the huge automotive companies 10% can still give the companies large enough budgets for innovation. A margin of 10% is a much smaller dollar amount available for the smaller construction companies to reinvest in innovation or any other need. These factors constrain prominent players from taking big bets to force radical shifts in the industry.

Capital-intensive, fragmented and geographically-spread

Automotive manufacturing and construction are capital- and resource-intensive but spread out differently. The majority of the trillion dollars for the automotive industry flows through the same few hundred automotive assembly and parts manufacturing plants in the USA. However, the trillion dollars in construction flow through the million homes, thousands of commercial buildings, a few thousand miles of road, and over a thousand bridges constructed yearly.

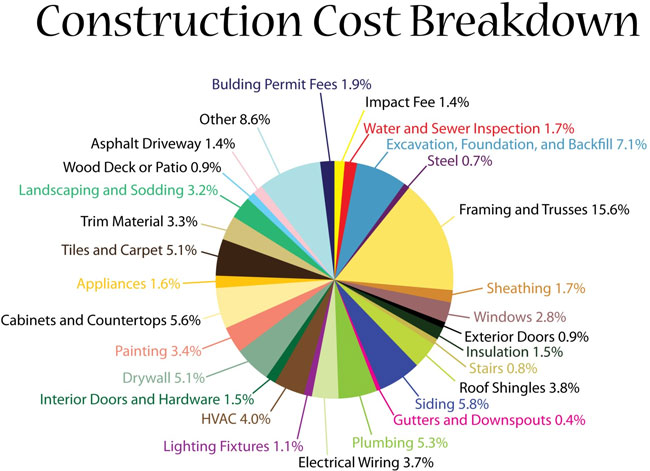

Many large general construction companies directly perform only a fraction of the direct physical jobs. They often contract most of these to subcontractors. To give you an idea of the number of different trades involved, here is a breakdown of the costs for a typical home:

Courtesy: helperhomes.com

Due to this subcontracting approach, millions of construction businesses(~3M) exist in the USA. For comparison, there are only 1.3M food small businesses in the USA. Radical improvement of onsite construction requires innovation in every trade shown above, and sophisticated workflow and coordination software.

Risk-averse

Although different tasks in construction have varying degrees of risk, the mentality of risk-averseness is prevalent. However, recent challenges such as high costs and labor shortages are creating a tremendous need and appetite for innovation.

Self-perform General Contractor

Self-perform GCs are well-positioned to reap the benefits of cost/time optimization from robotics. But only some GCs do self-perform. Also, not all self-perform GCs perform everything in-house. They often subcontract jobs. We see this specifically for rebar and concrete work.

It may not be possible to automate all trades, so it’s essential to prioritize the first ones for automation. Further research is needed on this topic, and I look forward to connecting with innovation team at self-perform GCs.

Challenges to adopting robotic solutions

The value propositions of robotic automation are usually one or more of the following:

- Lower cost

- Lower labor cost and delays from absenteeism and limited labor availability

- Faster task and project completion

- Safer work environment as machines take on dangerous human tasks

- Error reduction because robots by design specialize in precision and task repetition

As discussed above, the construction industry differs from other industries, but certain aspects prevent startups and new ventures from entering and succeeding in construction robotics. Adoption of robotics products requires technological feasibility and commercial and workflow viability.

- There is quite a bit of chaos/uncertainty/unknowns at the construction site for many reasons; One is that various trades access a common space simultaneously. Various trades have to coordinate, which is quite challenging due to the social and uncertain nature of the interaction. Because of this lack of order, the workflow of current robotics systems is not readily adaptable to the construction industry. Until now, cookie-cutter-style tasks are the most suited to robotic automation. Recently, with the development of advanced computer vision and control algorithms, there has been a push to develop automated solutions that go beyond the “do one task on one type of object” to “do multiple tasks on a wide variety of objects”. Still, the technology needs to mature more for ubiquitous adoption.

- Although large enterprises have sufficient resources to survive through long product development cycles, startups must live through the valley of death. They often rely on the Robot-as-a-Service (RaaS) model to capture revenue by providing services instead of selling products at a lower Technology Readiness Level, TRL. Higher TRL products/equipment are disproportionately more expensive to build. But RaaS is hard to scale and operate in construction environments where schedule changes from weather and design errors could negatively impact the operating margin, especially when they are already low. For example, if a RaaS offering that was supposed to be completed in a day got delayed by an extra day due to rain, the onsite cost doubled. Employees have to be paid even if it’s a rainy day. The weather contingency plan is integral to the construction schedule, and rain-days are intentionally added as a buffer. These often come to the rescue if schedule delays occur in fair weather.

- Since most humans don’t do just one thing, adopting a task-specific automation solution is challenging since the unit economics to replace n number of people is difficult to calculate. Humans also perform exception handling quite well, so a system completely devoid of humans is not feasible since exception handling is not a strong forte of robotic systems. Collaborative robots, or cobots, are an easier way to automate with robots. However, assessing the economic feasibility of cobots can be a complex task, and incremental improvements may not be enough of a savings or improvement to establish clear winners. For example, imagine a robot costing $100k which helps to double the speed of a worker costing $100k a year. If it still requires the worker to operate the robot, the first year of investment in the robot plus wages for the worker cost $200k. Further, there is still the additional risk of new technology. As a project manager, the safe and easy alternative to speed up the job would be to hire a second person. This flexible alternative gets the job done this year, albeit, without the longer term benefit of the investment in the robot, and provides resources to perform others next year.

- Subcontractors are typically smaller in size. The idea of investing in new technology or assuming associated risks may not be appealing to many subcontractors. General Contractors(GC) could “inspire” their subcontractors to adopt robotic automation. GCs may not be incentivized to enforce automation on their subs if the value proposition is solely cost-saving; Cost benefits don’t trickle up. However, speed improvements and tighter schedules could be specifically bid for at a higher cost.

- Fast-track construction is a technique introduced to reduce time-to-completion. The construction starts even before the details of the design are finished. This results in uncertainties on the site when multiple trades are involved. Subcontractors may delay finalizing the design details to get the “as-built” changes on the site to avoid numerous corrections and coordination ahead of time. Many of these processes may look haphazard and are tasks only humans can do.

- It is often hard to get employees to buy into a new technology due to additional overheads it may create, job security risks, or simply the resistance to change. Minimizing the changes of workflow makes it easier to adopt new tech. Single tasks that do not need multiple trades to coordinate are easier to automate.

- Lastly, onsite construction is a hard job. In an economy where work-from-home is normalized, people in construction spend much time away from home: onsite, on the road, waiting, in hotels, etc. Companies looking to innovate in the onsite robotics space must hire and maintain a hardworking technical team enthusiastic about working in offices and on sites. The sun and the weather are not kind to human emotions.

The above challenges may be manageable when the value propositions reach the 5-10x scale. This scale enables the contractors to outbid the competition, complete jobs faster, and have a snowball effect.

On a positive note, numerous robotics solutions have been introduced to the industry recently despite these challenges, highlighting the urgent requirement for automation in this field. Stay tuned for upcoming articles on successful strategies in this space.